{kind=link}

With less than three weeks until the U.S. presidential election, millions of Americans say the economy is a top issue as they decide how to cast their vote — an understandable focus after the rollercoaster of the past four years, which included everything from a bear market to the hottest inflation since the 1980s.

But with the chaos of the pandemic behind us and inflation edging close to its pre-2020 levels, the U.S. economy is ripe for a fresh assessment of its strengths and weaknesses, along with whether the Biden administration’s economic policies have paid off.

By many measures, the U.S. economy has regained its footing, emerging from the health crisis with the type of growth that it experienced prior to 2020. Gross domestic product is growing solidly, while unemployment and the labor market have also rebalanced, remaining close to their pre-pandemic levels. Critically, inflation has dropped to a three-year low and is approaching the Federal Reserve’s annual target of 2%.

To the surprise of many forecasters, that rebound occurred even as the Fed boosted interest rates to a 23-year high in an effort to cool inflation. Historically, such rate hikes have often led to recessions. But so far, the U.S. has avoided a downturn, and instead appears heading for a “soft landing,” or when the economy continues to grow and the job market remains strong despite the headwinds of higher rates.

“In the 35 years I’ve been an economist, I’ve rarely seen an economy performing as well as it is,” Mark Zandi, chief economist of Moody’s Analytics who has previously advised presidential candidates from both parties, told CBS MoneyWatch. “I’d give it an A+.”

Like Zandi, many other experts are giving the economy strong marks. The U.S. economy is “hot, hot, hot,” noted Yardeni Research in an October 17 report. The job market is “resilient” and “there is no quit in the U.S. consumer,” analysts at Oxford Economics told investors this week.

Yet many Americans might scoff at such bullish assessments: 6 in 10 now describe the U.S. economy as either “fairly bad” or “very bad,” according to CBS News polling.

That’s not lost on Zandi and other economists. “The difference between the happy talk of economists and what people say has never been this wide,” he noted.

Why Americans give the economy poor marks

Only 1 in 10 Americans rate the economy as “very good,” according to CB News poll of registered voters taken between October 8-11. Meanwhile, about 52% of Americans say they and their family are worse off today than they were four years ago, Gallup found in a new poll.

“Despite recent economic data suggesting the labor market, consumer spending and the overall economy are proving to be very resilient and strong, consumers’ sentiment about economic conditions and future prospects remain downbeat,” Kathy Bostjancic, chief economist at Nationwide, told CBS MoneyWatch.

The discordant economic views among experts and typical Americans reflects several factors. First, and perhaps most pressing in the short-term, prices around the U.S. remain elevated even as the searing inflation that followed the pandemic descends to normal levels.

Second, economists tasked with the complexity of deciphering a $29 trillion economy naturally rely on broad metrics such as GDP, the Consumer Price Index and the nation’s unemployment rate.

Yet such data, even when bolstered with consumer confidence surveys and other public sentiment measures, don’t capture the far more nuanced financial realities facing households. For many Americans, their perceptions are shaped less by fluctuations in growth rates or monthly job gains than by the more palpable daily struggle to pay for food, rent and health care.

Third, mounting inequality in wealth and income has made successive generations of Americans more vulnerable to economic crises at the same time that traditional financial milestones, such as owning a home, become harder to achieve.

Finally, polling suggests that political polarization is significantly coloring people’s views of the economy. In such an environment, a sharp disconnect between what the economy looks like on paper and how people experience it is not only unsurprising, but perhaps inevitable.

An educational and party divide

Indeed, there are maor partisan and educational divides in how people assess the economy, CBS News polling shows. For one, Republicans are much more likely to give the economy poor marks than Democrats, a reflection of partisan views about the direction of the nation.

“If you are Republican, it doesn’t matter what you say — they don’t think the economy is good,” Zandi noted.

Almost 9 in 10 conservatives describe the economy as bad, compared with 3 in 10 people who lean liberal, CBS News polling found. If former president Donald Trump wins in November, Zandi predicts that sentiment about the economy will shift, with liberal-leaning voters suddenly souring on the economy and conservatives becoming more upbeat.

But there’s another divide that points to the longer-term inequality issues in the U.S.: a gap between people with and without college degrees. Americans without a bachelor’s degree are much more negative about the economy than those with a college education — a disparity that may point to decades of lagging wage growth for workers with only high school degrees.

For instance, 47% of White voters with a college degree describe the economy as good, compared with 29% of those without a diploma, an 18 percentage-point gap, CBS News polling found earlier this month.

Americans with college degrees have seen their income and wealth surge during the past several decades, leaving non-college educated workers behind. The disparities are particularly acute for young men without a bachelor’s degree, with Pew finding that this group earned median incomes of $45,000 in 2023 — 22% less than the same group in 1973.

Those workers are feeling the sting of inflation the most acutely, Zandi said. “Grocery, rents, gasoline took off largely because of the pandemic and the Russian war, and those are things that you need and are a good part of the budget of lower-income households, who are lesser educated.”

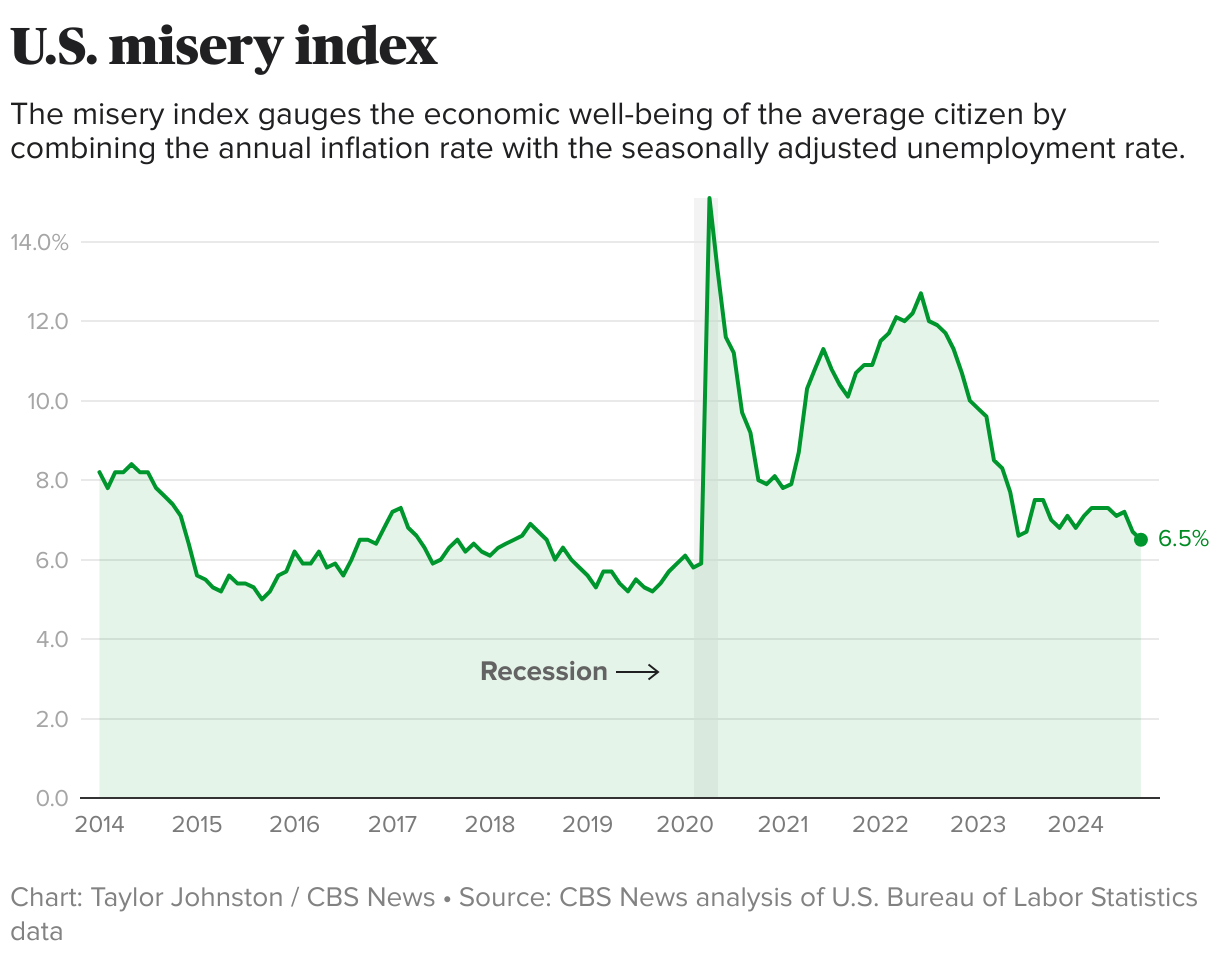

The “misery” index

Another way to measure the economic realities of Americans is the so-called misery index, which represents the sum of the unemployment and inflation rates. The idea is that higher unemployment and inflation will lead to more unhappiness, while lower rates will reduce suffering.

The misery index, an informal measure followed by economists, stood at 6.5% in September, below its average since 1947 of 9.1%, Ed Yardeni of Yardeni Research noted in a recent report.

“Should consumers be happier?” Yardeni asked.

Maybe, but Yardeni pointed out that Americans are responding to more than the inflation rate and the health of the job market. Americans also face many other financial pressures, ranging from high borrowing costs due to the Federal Reserve’s interest-rate hikes to a feeling of “precarity,” especially among younger voters who are struggling to buy their first home or pay college loans — issues that aren’t tracked by the misery index.

Older Americans, meanwhile, have greatly prospered from higher home values and a stock market that continues to hit new highs, but half of them are also financially supporting their adult children, Yardeni noted.

“On average, parents providing financial support give $1,384 to their children monthly,” he said. “That’s more than twice what the average working parent in the study contributed to his/her own retirement savings monthly.”

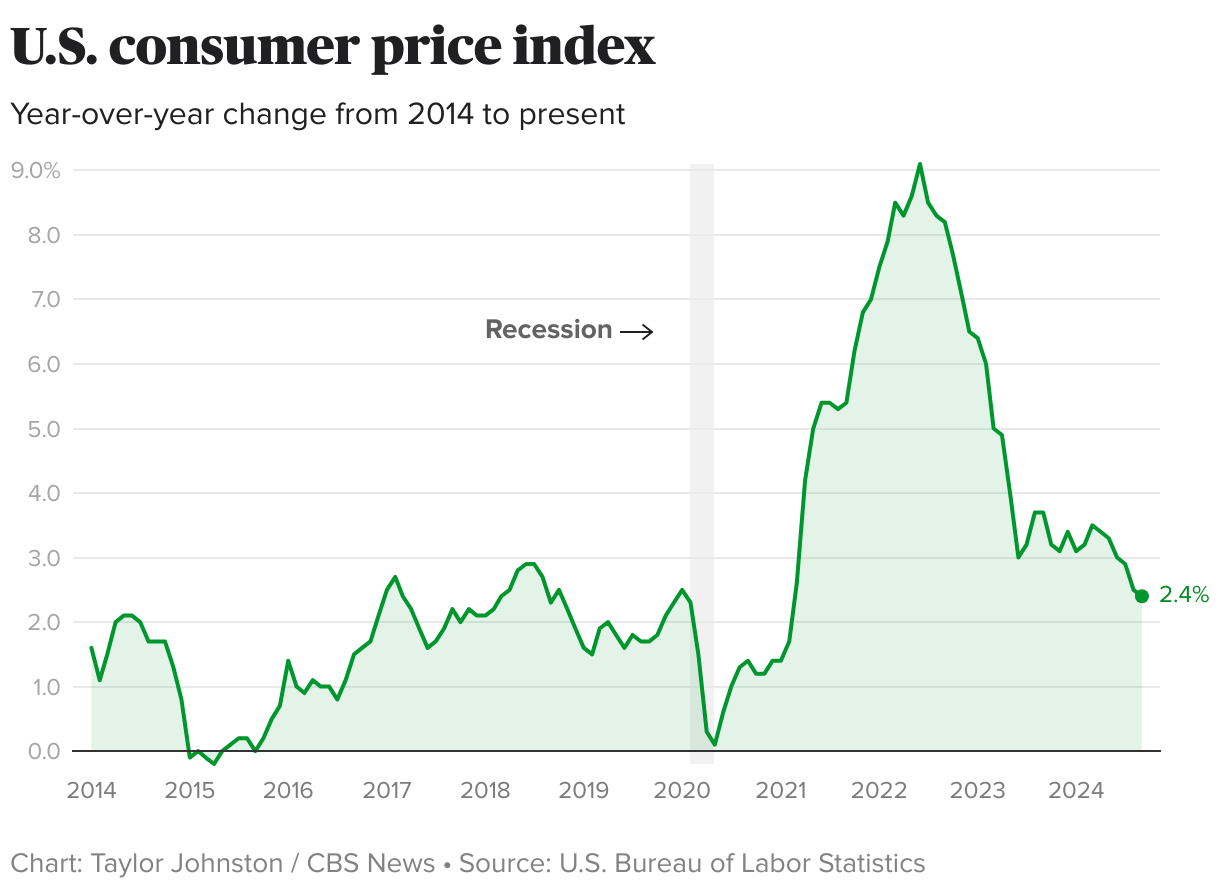

Lower inflation, higher prices

Inflation, meanwhile, has dipped to a three-year low, hitting 2.4% in September, the most recent Consumer Price Index shows. That’s not far from the Fed’s goal of driving it down to 2% on an annual basis, opening the door to the central bank’s September rate cut, its first since the start of the pandemic.

But despite the Fed’s jumbo 0.5 percentage point cut last month, borrowing remains expensive, including for mortgages, which has priced many homebuyers out of the market.

“The reasons for the sour outlook are rooted in the prior surge in inflation that has greatly lifted the level of prices for goods and services, including for homes and rents, and the still-high interest rate burdens facing particularly lower- and middle-income households,” Bostjancic said.

For instance, groceries still cost 26% more than in January 2020 just prior to the pandemic, a painful hit to the wallet whenever consumers stock up on food.

“Almost everyone has a food item they purchase on a regular basis they use as a litmus test for everything they view about economy, and they are paying more than they did four years ago,” Zandi said. “A pound of sugar, ramen noodles — even though the price of those things haven’t risen much over the last year, they are 20-25% higher than they were four years ago.”

Prices “aren’t going back to what they were,” he added. “That’s what people feel.”

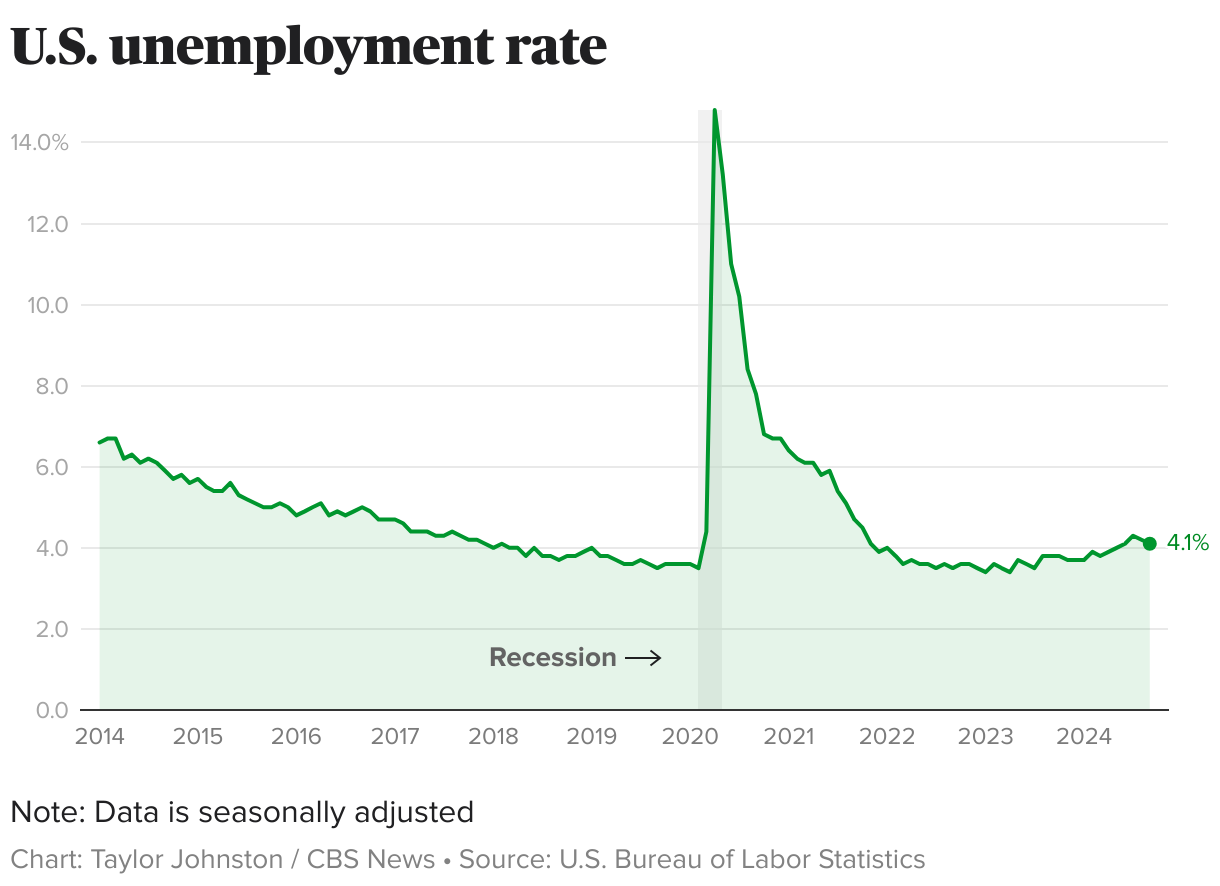

Employment and wages

The U.S. unemployment rate remains near a 50-year low, although it has inched up slightly in recent months, which is one reason the Fed opted to cut rates last month.

Hiring is slowing but remains relatively strong, with employers adding 254,000 jobs in September, blowing away economists’ forecasts. The U.S. is creating about 150,000 to 175,000 new jobs per month on average, Zandi said, which he described as “extraordinary.”

“When you look at forecasts before the pandemic of job growth, it would be 75,000, not 150,000,” he noted.

Meanwhile, workers’ wages have edged ahead of inflation since May 2023, giving employees some relief. But it might not be enough to offset the pain of high prices.

“Even though income levels for households have also increased, many times catching up to the rise in inflation, consumers still reel at the sticker shock of higher prices,” Bostjancic said.

Stock market at record highs

While the stock market doesn’t reflect the economy, rising asset prices have helped lift the financial fortunes of millions of Americans. This year, the S&P 500 has repeatedly hit record highs, providing gains to the 401(k) plans and investment accounts of workers and retirees alike.

But only 6 in 10 Americans own stocks, according to Gallup, and more than half of workers lack access to an employer-sponsored retirement plan.

Those Americans “aren’t benefiting from record stock prices,” Zandi said.

Many are unaware that the stock market has reached record heights, with only 4 in 10 Americans telling CBS News that equity prices are higher than at the start of the year. About 3 in 10 say it’s lower or the same, while another third say they’re unsure.

“I have this metaphor in my mind that the economy is like an elephant, and depending on what you part you touch you can get a different sense” of what it is, Zandi said.